NewRetirement PlannerPlus Retirement Calculator

This site may be best known for retirement calculator reviews, including the most comprehensive collection of retirement calculator reviews on the web. Ultimately, we would love to find “the one” perfect retirement calculator for everyone.

Unfortunately, that perfect retirement calculator doesn’t exist. We all have unique preferences, needs, and desires. It is important to find the right tool to meet your needs.

Earlier this year, Darrow reviewed the Pralana Gold 2020 Retirement Calculator. Today, I’ll review NewRetirement PlannerPlus.

Read on to learn the differences between these powerful financial planning tools and which may be the better fit for your retirement planning needs. I’ll then walk you through some of my favorite features of NewRetirement’s PlannerPlus.

Comparison Shopping

Before diving into the NewRetirement PlannerPlus review, let’s compare a few key differences between these two powerful retirement modeling tools to help you decide which may better fit your needs.

| Feature | NewRetirement PlannerPlus | Pralana Gold |

|---|---|---|

| Application | Web Based | Microsoft Excel |

| Support | In program prompts and feedback, chat/email, Facebook group, option to upgrade to personal assistance | Online manual, email, online forum (coming 2021) |

| Modeling | Average returns, Monte Carlo (Beta version) | Average returns, Historical returns, and Monte Carlo |

| Updates | Constant, iterative | Annual, updates require download |

| Cost | $72/year | $99 initial purchase, $49 annual upgrade |

Ease of Use

A few features make NewRetirement’s PlannerPlus tool attractive. Using a web based interface means you can start using it immediately and access your scenarios by logging into almost any device. In contrast, Pralana needs to be downloaded to a device (license allows download to up to 3 devices) and requires Microsoft Excel to run.

If using multiple devices, you simply log into your NewRetirement account to access your information. Pralana Gold requires exporting and importing data from device to device.

NewRetirement’s slick user interface and outstanding customer support each shorten the learning curve. PlannerPlus provides ongoing assistance and feedback in a variety of ways. This includes in-app help and links to off-site resources.

These resources provide information as the user needs it. This approach provides convenience and helps insure more accurate data collection, which is vital to get the most valid and useful output possible.

“Coach suggestions” help identify inputs that seem questionable or could be optimized. There is also a chat window, an active NewRetirement Facebook group and occasional webcasts where users can interact with PlannerPlus developers and other retirement experts.

You can also upgrade from the base PlannerPlus to PlannerPlus Live and have someone individually walk you through the program, review your plan, and answer personal questions.

In contrast, Pralana requires referring back and forth between the program and a user manual. Pralana does offer email support directly from the developer and is planning to launch a user forum starting in 2021.

This makes for a slightly longer learning curve with Pralana Gold. It also requires more technical and financial planning competence and confidence from the user.

Modeling

Both the NewRetirement PlannerPlus and Pralana Gold retirement calculators start with basic inputs and quickly provide useful outputs to give you an overview of your financial picture.

Each then prompts you to enter detailed personal and financial inputs which lead to detailed outputs. Beyond helping you answer the basic question “Do I have enough money to retire?” these are both advanced personal financial modeling tools with ability to model withdrawal strategies, federal and state income taxes, Roth conversions, healthcare expenses and much more.

An advantage of Pralana Gold is that it provides outputs based on average returns, historical returns and Monte Carlo simulations. NewRetirement provides outputs based on average returns. They recently launched a beta version using Monte Carlo simulations in PlannerPlus.

There is no “best way” to model outcomes. Each method comes with its own advantages and drawbacks. More outputs are generally better for those who want a broader picture of the range of possible outcomes.

How and Why Behind the Calculators

Understanding the background of the creators of these calculators, the motivations for creating them, and how they continue to improve these tools can help determine which may be a better fit for your retirement modeling needs.

NewRetirement PlannerPlus is web based. Their team’s strategy is to release new features frequently, get feedback from users, and incorporate the feedback quickly as the team continuously improves and upgrades PlannerPlus.

This model is a reflection on the mindset of founder Steve Chen and his team at NewRetirement. Chen started NewRetirement after struggling to assist his mother navigate her finances. He created an affordable and user friendly product for people interested in their personal finances, but who need help navigating the complexity. Chen’s goal is to revolutionize retirement planning by creating a detailed and accurate tool that is accessible to the widest possible audience.

Pralana founder Stuart Matthews is a retired engineer. He is a one man team who started Pralana to scratch his own itch in retirement. He wanted to create powerful and accurate retirement planning software that didn’t previously exist for serious DIY planners at a reasonable cost.

Matthews turned his creation into a business, creating a cult-like loyalty among highly financially literate DIY planners who want the most powerful computational tool with the ability to model complex and specific scenarios.

He is extremely detailed and works on perfecting updates to the calculator which he releases once a year to introduce new features and update contribution limits, tax brackets and other changes in the law. Updating requires renewing your license annually and downloading the newest version, exporting your data from the previous model, and importing it into the newest one.

Cost

As I’ve hopefully made clear, these are both valuable and powerful retirement planning tools. Each fills a need for different subsets of our readership. Fortunately, both are tremendous values.

Before discussing the price of these tools, I want to point out that both have free versions. NewRetirement offers the free NewRetirement Planner. Pralana offers the free Pralana Bronze.

Both of the free versions are valuable if you are looking to get a rough estimate of your financial position. They also give a good feel for how the paid versions look, feel, and work. Neither is in the same league as the paid version for those who want to get serious about detailed financial planning projections.

DISCLOSURE: Can I Retire Yet? is an affiliate partner with both NewRetirement and Pralana. As such, if you purchase either calculator through the links on this website we are paid a portion of the purchase price. This allows you to support the blog without increasing your cost. We are proud to be associated with both of these products.

NewRetirement PlannerPlus costs $72/year. You can upgrade to PlannerPlus Live for $125, which gives you access to live support. NewRetirement also gives the option of reviewing your plan with a Certified Financial Planner for a flat fee of $500.

Pralana Gold costs $99 when you purchase. Annual updates to the software are $49 after the initial purchase.

NewRetirement PlannerPlus

Darrow recently reviewed the Pralana Gold 2020 calculator. If you’d like to learn more about this powerful tool, you can read his full review.

For those of you that find the NewRetirement PlannerPlus more intriguing, I’ll walk you through how you get started with it and point out a few of my favorite features.

Onboarding

NewRetirement PlannerPlus has you start with a quick onboarding process. You enter basic information which takes only a few minutes and you quickly get a rough idea of your financial position. Inputs include:

- About You: Simple entries of your name, age, marital status, spouse’s info and retirement goals.

- Income: Gross pre-tax earned income (self and spouse), desired retirement ages, SS benefits & planned starting ages, and pension income and starting age (if applicable).

- Assets: Retirement savings and ongoing contribution amount and frequency, other savings, home ownership status, home value, and mortgage balance.

- Expenses: Mortgage payment and interest rate, medical expenses, & other expenses.

- Health: Answer a few questions about whether you’re a smoker, what Medicare coverage you anticipate having, and LTC plans.

After entering these quick inputs you’ll be taken to the Dashboard, where you’ll get an overview of your financial picture, discover ways to improve your plan, and learn more about key planning decisions.

NewRetirement Dashboard

At the top of the dashboard screen you will see key outputs based on the information you’ve entered. Outputs include your:

- Overall score that reflects the odds of meeting your goals based on your inputs and assumptions,

- Current net worth,

- Estimated monthly retirement income,

- Estimated estate value (reflected as a negative number if you aren’t projected to have enough money to meet your needs),

- And estimated age when savings will be exhausted.

In the dashboard, you can easily toggle between optimistic vs. pessimistic assumptions, assumptions based on your ideal budget vs. only expenses you define as necessities, and different withdrawal scenarios. This quickly and effectively demonstrates the wide variability of outcomes possible when even small changes in assumptions or inputs are compounded over time.

You can later create up to five additional scenarios to imagine and compare different potential retirement outcomes.

PlannerPlus — My Plan

Your next step is to enter detailed inputs to give a more accurate and nuanced look at your financial situation. All of the inputs are easily found under the My Plan tab. You can enter your information over multiple sessions and update it easily at any time.

We won’t cover every input option, but I will highlight a few key features under each section to give a sense of the degree of detail possible and features I found helpful.

Basic Profile and Goals

One key variable in retirement planning is life expectancy. This is unknown for all of us, so I would look up average life expectancy or use a generic number.

NewRetirement provides an in app link to a life expectancy calculator that has you enter variables such as your current age, health status, family history, and behaviors to give you a personalized number.

While you can’t know with certainty when you will die, this personalized number may give you more insight. After seeing my results, I increased my life expectancy assumptions.

Work and Other Income

PlannerPlus has you enter your gross income and assumed rate of increase. It then does detailed federal and state tax calculations. It also allows modeling of passive income including real estate, royalties and franchises.

Social Security

PlannerPlus links out to the MySocialSecurity website to make it easy and convenient to find your information. It also provides multiple resources about SS rules and claiming strategies to help you develop the optimal claiming strategy.

Annuities and Pensions

PlannerPlus enables modeling of annuity income and includes an annuity calculator and annuity suitability quiz to help you make a more informed decision about incorporating an annuity into your retirement plan.

The program also allows modeling of either monthly pension income or a lump sum pension.

Savings and assets

PlannerPlus provides simple and intuitive inputs allowing you to model:

- Tax advantaged accounts (tax-deferred, Roth, HSA, 529) and taxable savings,

- Roth conversions,

- Ongoing savings, and lump sum investments such as an inheritance or selling a home,

- Growth of private business value and/or a lump sum investment when selling the business.

Withdrawals

PlannerPlus models withdrawals based on spending needs and maximal withdrawals while still meeting legacy goals, and compares each to fixed percentage withdrawals. You can also model any number of one time expenses in the year you anticipate them, such as paying for a child’s college.

Expenses and Inflation

You can model expenses as a single monthly total or use the Budgeter tab, which lets you enter expenses with as much specificity and detail as you like. I prefer the Budgeter both for the amount of detail it enables and as a checklist to avoid forgetting any categories of spending.

Another great feature is the ability to label each expense as “must spend” or “like to spend” and then be able to toggle back and forth to see the difference in outcomes between the spending you would desire and a pared down budget with one click of a button. This is a great way to visualize the impact of spending decisions.

Home and Real Estate

I’ve written about the myriad of planning options that come with the decision to own a home. PlannerPlus allows you to model these options and see the financial implications.

This section allows you to model owning your home outright, carrying a mortgage, or renting. It also enables modeling a reverse mortgage, relocating, and buying or selling additional properties. When you enter your state of primary residence, PlannerPlus will then also use that information to model state income taxes.

My posts about relocating in retirement have been popular with a lot of readers, and domestic geoarbitrage has been a topic with several readers I spoke with over the past couple of months. NewRetirement PlannerPlus is a great tool for modeling different scenarios such as downsizing or moving to a state with higher or lower housing costs or state income taxes.

Medical

This section enables you to model both health insurance premium and out-of-pocket expenses. It also enables you to experiment with different inflation rates than you use for other expenses, which is wise considering that medical costs typically increase at a greater rate than general inflation.

Other inputs include the ability to model long-term care needs. There are also tips and links to resources relating to all of these topics as well as Medicare expenses to help you model your situation as accurately as possible.

Debts

This section allows you to model non-mortgage debt. It also provides resources to help you consider the impact of entering retirement with debt and options to pay your debt off more quickly.

Estate Planning

This section prompts you to consider the potential of leaving a legacy and provides resources about leaving a legacy. There is also a checklist to help you assemble and maintain documents for a comprehensive estate plan.

More Than a Calculator

I have gone through the inputs to give potential users an idea of what the tool can do and the level of detail it enables. I’ll highlight just a few outputs and highlight more of them in future blog posts when I model scenarios as I explore different concepts.

I want to point out that NewRetirement PlannerPlus is more than a retirement calculator that takes in and spits out numbers. What I really like about PlannerPlus is that it is a comprehensive retirement and general financial planning tool.

The access to resources, checklists, and tips to help you gather and enter more accurate data and then optimize your plan will allow many DIY planners to have more confidence in their plans. People who use or are considering using a financial advisor will gain more insights and confidence, enabling them to ask better questions of the advisor and more accurately assess the advice and quality of service they’re receiving.

I mentioned this earlier, but it bears repeating. This tool performs all of these powerful functions without overwhelming the user. The tool is very intuitive and the ability to jump right in and start playing with it makes it fun… at least for a geek like me who likes thinking about things like the impact retiring sooner has on tax minimization and Social Security benefits.

Outputs

NewRetirement PlannerPlus takes the inputs you enter and gives a lot of useful outputs. I’m going to highlight just three that will give a sense of the information you get and how it can impact your planning.

Dashboard

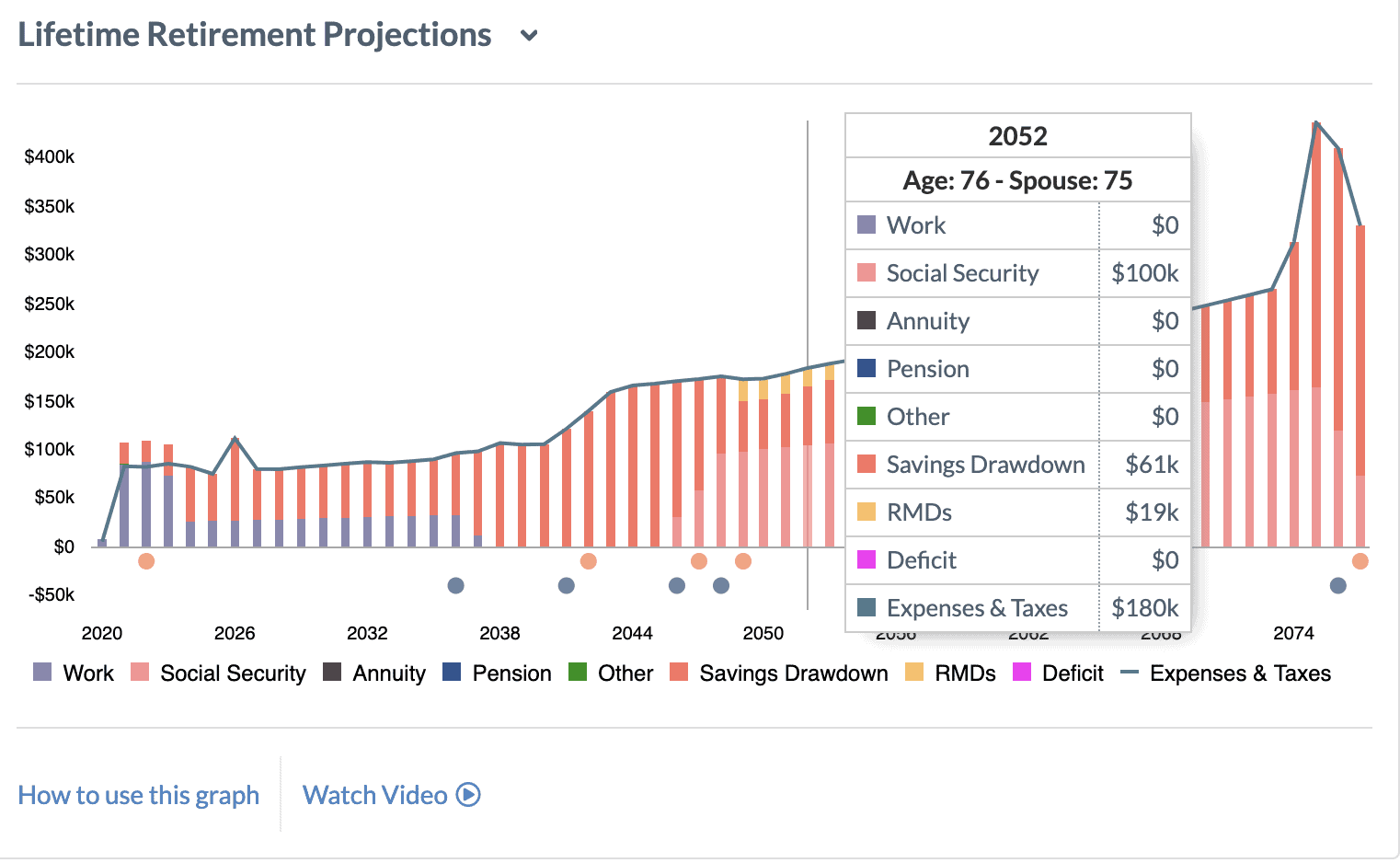

In the dashboard, your Lifetime Retirement Projections are on display in a clear easy to understand bar graph. You can hover over any specific year, and see a breakdown of year-by-year cash flows to meet your projected inflation-adjusted spending needs.

As an example, in the picture above from a scenario I created you can see the following:

- In this example, I hovered over the year 2052. It shows living expenses and taxes total $180,000 which would be met by $100k Social Security (light pink), $19k RMD (gold) and $61k from other savings drawdown (dark pink) .

- In the early years, part-time work (represented by the color purple) covers most spending needs and is supplemented by savings drawdown (dark pink).

- The next 12 years model a small income from decreased part-time work (purple) and most expenses being funded by savings drawdown (dark pink).

Insights

Under the Insights tab from the Dashboard, PlannerPlus analyzes:

- Savings timeline,

- What you need,

- Cash flow forecast, and

- Net worth and estate.

The PlannerPlus Inspector provides intuitive visual representations of your lifetime:

- Income and expenses,

- Savings,

- Taxes,

- Withdrawals, and

- Surplus or Gap

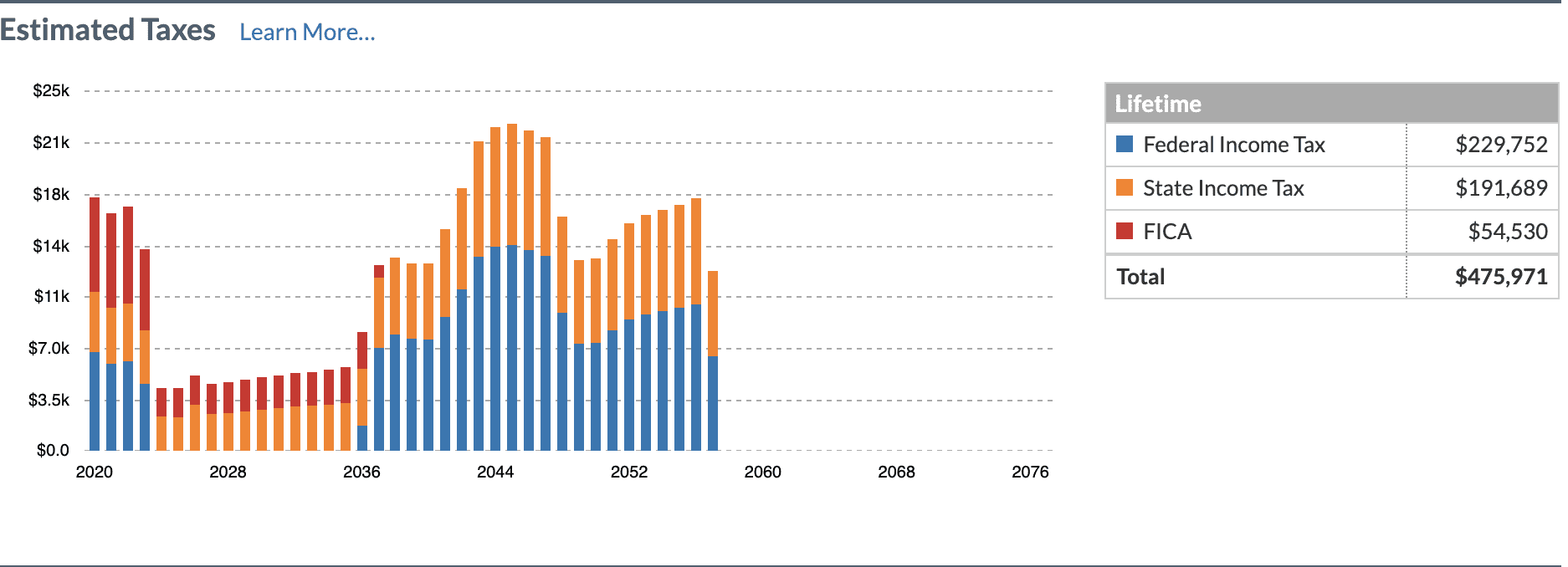

I’ve included a screenshot of the tax inspector from a scenario I created where one spouse works a few more years until 2023, then they have only a very small earned income in early retirement through 2035. You can easily see that this would provide a twelve year window where the couple would pay no federal income tax (represented by blue bars). This would present an excellent opportunity to convert funds from a traditional to Roth IRA in the lowest tax brackets, potentially saving tens of thousands of dollars in federal income tax over the couple’s lifetimes.

How To Improve

PlannerPlus Dashboard also has a How To Improve tab. Here you will find general strategies to strengthen your retirement plan, depending on your goals. Strategies are divided into:

- Don’t Run Out of Money,

- Prepare for Risks and Unknowns, and

- Maximize Your Wealth

This section of the program also stores individualized “coach suggestions” based on your data inputs and links to resources on topics about which you requested further information as you were entering data. You can then learn more and go back and improve your plan based on new strategies as you learn.

You can also find links to resources on a variety of retirement planning topics, ways to connect with a fee-only Certified Financial Planner, and information on live online events NewRetirement hosts periodically to assist users.

Try It Now

NewRetirement PlannerPlus is a powerful and easy to use retirement calculator and much more. PlannerPlus is outstanding if you are looking for a way to integrate all of your information into one user friendly tool to create a comprehensive financial plan.

It allows you to test different planning scenarios, model cash flow and tax consequences of your decisions, and provides resources and feedback to increase confidence in the completeness and accuracy of your plan.

Give it a try and share your feedback.

* * *

Valuable Resources

- The Best Retirement Calculators can help you perform detailed retirement simulations including modeling withdrawal strategies, federal and state income taxes, healthcare expenses, and more. Can I Retire Yet? partners with two of the best.

- New Retirement: Web Based High Fidelity Modeling Tool

- Pralana Gold: Microsoft Excel Based High Fidelity Modeling Tool

- Free Travel or Cash Back with credit card rewards and sign up bonuses.

- Monitor Your Investment Portfolio

- Sign up for a free Empower account to gain access to track your asset allocation, investment performance, individual account balances, net worth, cash flow, and investment expenses.

- Our Books

- Choose FI: Your Blueprint to Financial Independence

- Can I Retire Yet: How To Make the Biggest Financial Decision of the Rest of Your Life

- Retiring Sooner: How to Accelerate Your Financial Independence

* * *

[Chris Mamula used principles of traditional retirement planning, combined with creative lifestyle design, to retire from a career as a physical therapist at age 41. After poor experiences with the financial industry early in his professional life, he educated himself on investing and tax planning. After achieving financial independence, Chris began writing about wealth building, DIY investing, financial planning, early retirement, and lifestyle design at Can I Retire Yet? He is also the primary author of the book Choose FI: Your Blueprint to Financial Independence. Chris also does financial planning with individuals and couples at Abundo Wealth, a low-cost, advice-only financial planning firm with the mission of making quality financial advice available to populations for whom it was previously inaccessible. Chris has been featured on MarketWatch, Morningstar, U.S. News & World Report, and Business Insider. He has spoken at events including the Bogleheads and the American Institute of Certified Public Accountants annual conferences. Blog inquiries can be sent to chris@caniretireyet.com. Financial planning inquiries can be sent to chris@abundowealth.com]

* * *

Disclosure: Can I Retire Yet? has partnered with CardRatings for our coverage of credit card products. Can I Retire Yet? and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. The site does not include all card companies or all available card offers. Other links on this site, like the Amazon, NewRetirement, Pralana, and Personal Capital links are also affiliate links. As an affiliate we earn from qualifying purchases. If you click on one of these links and buy from the affiliated company, then we receive some compensation. The income helps to keep this blog going. Affiliate links do not increase your cost, and we only use them for products or services that we're familiar with and that we feel may deliver value to you. By contrast, we have limited control over most of the display ads on this site. Though we do attempt to block objectionable content. Buyer beware.

Hi Chris,

I didn’t read your article yet, but the title of the article triggered my memory and a question I had.

I recall the review from earlier this year. There was some pushback from the people’s comments (including myself I think) due to some conflict of interest and purported promotion of the tool. Is it the main reason why neither of you (Darrow and you) haven’t written any instructional articles on how to use Parlana’s tool? Unless I forgot entirely, I think there was such a promise within that article. So, even though it sounded like a promotion at the time, I also thought to myself, “Well, if they really write a very good instruction with some examples, I might try it our myself.” However, I haven’t seen such an article yet, am I right? Or have you both decided not to do it after all?

TY

S&M,

That was our intention at the time, and remains so to a point. Darrow did write an article in March about When to Take Social Security and explained how he used the Pralana Gold to assist his analysis.

Since then, our world was flipped on its head and a lot of things we thought we would be writing about have changed. I didn’t anticipate writing about processing the uncertainty in the world created by the pandemic, rebalancing a portfolio that dropped 30% in a couple of weeks, or dealing with depression, but those are among the topics I’ve published on in this crazy past couple of months.

So back to your original question, yes I would anticipate more articles like the one Darrow published in March where we highlight how to use these tools to help solve real world retirement problems. I just don’t guarantee when, which calculator, or on what topics, as the writing on this blog represents what we’re personally thinking about and working on at the time, or responding to reader questions.

If you have a topic you’d like to see addressed, feel free to ask and I’ll do my best to respond personally or in the form of a blog post if I think it is a question that could help others.

Best,

Chris

Hello,

Could this Retirement planner be sub tailored for another country? i.e. New Zealand?

We have a more socialist Govt with a deal of healthcare being the responsibility of the Government, and not as much requirement for personal Healthcare policies.

thanks.

Christine,

Both of these tools are tailored for American users. In addition to modeling healthcare, which is different in the States than most places, one of the best features of both of the calculators mentioned is detailed modeling of U.S. and state tax codes. As noted in the article, both have free versions. You may want to experiment with each of those and if one of the calculators is more appealing, reach out to the developer with specific questions about modeling country specific issues such as health care and the tax code before upgrading to the paid version.

Best,

Chris

I didn’t see anything about security/privacy. If I’m giving them personal info the security has to be spotless. What’s your take on how they handle security/privacy issues?

Excellent question Jims,

I personally use both of these calculators. Privacy is a big deal to me and I wouldn’t recommend anything to readers that I wouldn’t personally use myself.

NewRetirement is internet based. You have to provide them with your email to sign up for an account. You can manually enter all of your information, so they can see the values you enter into the calculator and use it to aggregate data such as average user net worth, etc. However, they have no personal information such as account #’s, institutions where you hold savings and investments, etc. You don’t even have to enter a last name.

Pralana also requires you to provide an email so they can send you a download code. Once you download that calculator, they have no access to even your account balances, let alone any personal information that could compromise your privacy.

In contrast, other companies use calculators as loss leaders to generate customer leads. One in particular, which I won’t name, pays bloggers very handsome commissions just to get people to sign up for their free calculator, which by all accounts is a very nice tool. However, it requires you to link your accounts, which makes me uncomfortable from a security perspective and I wouldn’t personally use. They then solicit users to sign up for expensive investment management services, using a fee model I don’t support. Therefore, we decided not to promote their tool.

The only way it makes sense to use an affiliate model as we are here is if it is a win for the reader (learn about a valuable product), win for the producer (sells more product to our audience) and win for me (make some money for connecting the other two parties).

Hope that clarifies how I approach these things.

Best,

Chris

It got me curious which product you’re referring to… I don’t read a lot of PF blogs, but I have noticed bloggers ‘encouraging’ their readers to sign up for Personal Capital account. Is this a good guess? I know that MMM used to promote Betterment and then stopped I think.

“One in particular, which I won’t name…” 😉

Hi Chris,

Well written! As a long-time user of Pralana Gold, as well as someone who spent several months testing New Retirement Planner Plus, I am sticking with Pralana Gold for now. Why?

As of the last version of NRP+ I was using, it still did not include Inherited IRAs as an account type (neither Trad or Roth). And the Roth IRA conversion tool is far more robust and useful within Pralana Gold. Both features for my planning needs are are critical. Perhaps someday NPR+ will be enhanced to address these functional gaps. I plan to give NPR+ another tryout to compare with the 2021 version of Pralana Gold.

Both Steve Chen and Stuart Matthews are great guys and have been very supportive of me with my use of their products.

Thanks,

Mike S.

Thanks for the helpful comment Mike S.

I agree that Pralana Gold has a few features that NewRetirement can not yet model that make it the superior tool for some users. On the flip side, NewRetirement is easier to jump right in and use and provides more assistance to users that makes it superior for others.

I’m happy to support both as they serve different segments of our audience. I also agree that both Steve and Stuart are great guys who are constantly trying to improve their products and I’m happy to support them both for that reason as well.

Cheers!

Chris

Retired Military here.. Does it a have a medical option for military retirees? military retirement or VA disability payments? thanks, Chris

Chris,

I’m not an expert on military benefits. So the answer would depend on how your benefits are taxed. If taxed the same as civilian benefits, there should be no issues and either tool should work fine.

There may be tax law differences that I’m not aware of. If that is the case and you have specific questions, it would be best to reach out directly to the creators of the calculator you’re interested in through their respective websites.

Hope that helps.

Best,

Chris

Didn’t read the whole article yet either, but noticed in your example you stated “it would be met with $100k of social security”. Are you trying to say that you are receiving $100k per year from social security? I have been under the impression that the most social security will ever pay someone is around $37k per year…please let me know…thanks!

Tracy,

That is many years into the future so that demonstrates the impact of inflation. It is also just a hypothetical example to demonstrate the outputs and is based on two individuals in a couple receiving 100% of benefits and claiming at 70 years old if I recall how I built out the scenario. You can build in a cut to your benefits if you don’t have confidence in the system that far into the future as many people don’t.

Best,

Chris

Does this NRP tool present results in nominal dollars only? I would have thought that it would be clearer to see in today’s dollars, no?

“Clearer” is subjective, so that depends on who you’re asking. I find it interesting to see the impacts of inflation when compounded over decades. It is simultaneously a bit startling to see that spending needs will be several multiples of what they are now. However, that is probably helpful to a lot of conservative investors with a long time horizon who think of volatility as equivalent to risk, when volatility is just one risk and inflation and longevity are others that need to be planned for.

The key thing is that inflation is accounted for one way or the other in calculations.

Best,

Chris

Hi, I have purchased NewRetirement Account

and I started with the link in this article.

Excellent review, and the tool looks really complete. Thanks.

I’m a long time reader of this blog and have gotten Darrow’s books. They helped me retire at 52.

thanks again,

BEN BUTLER

Thanks for the feedback Ben. Best wishes and happy to hear any feedback after you’ve used the calculator a bit.

Best,

Chris